A Guide to Tax Year End 2022/2023

With every tax year, it is important to make sure you are in the best possible financial position to protect and grow your future wealth.

Our latest guide to year-end tax planning provides you with the dates you need to be aware of, as well as details of the allowances and reliefs available, to put you in the strongest financial position.

This guide is aimed at personal customer. Tax rates for commercial customers and trustees may differ.

D E A D L I N E S / D A T E S

The UK tax year spans a 12-month period, starting on April 6th each year and ending on April 5th the following year. The 2022 tax year therefore runs from April 6th, 2022, to April 5th, 2023. Here are the other important dates you need to know:

PERSONAL ALLOWANCE: £12,570

The tax-free personal allowance for the 2022-2023 tax year is £12,570. This has been frozen until 2028.

This is the amount you are able to earn before you have to pay any tax. If you live in England, Northern Ireland or Wales, any amount you earn that exceeds this will be subject to taxation at the following rates.

• 20% basic-rate: £12,571 - £50,270

• 40% higher-rate: £50,271 - £150,000

• 45% additional rate: £150,001+

Your Personal Allowance goes down by £1 for every £2 that your adjusted net income is above £100,000. This means your allowance is zero if your income is £125,140 or above.

STARTING RATE FOR SAVINGS: £5,000

The starting rate for savings for the tax year 2022-2023 (from April 6th, 2022, to April 5th, 2023) in the UK is 0%.

This means that if your savings income (which includes interest from bank and building society accounts, bonds, and unit trusts) is less than or equal to the starting rate limit, you will not have to pay any income tax on that income.

The starting rate limit for the tax year 2022-2023 is £5,000. This means that if your total income, including your savings income, is less than or equal to £5,000, you will not have to pay income tax on your savings income.

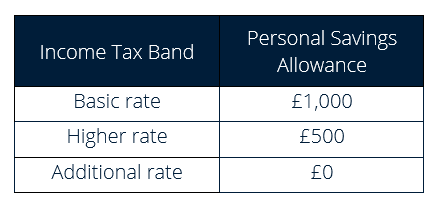

PERSONAL SAVINGS ALLOWANCE: £1,000

Depending on which ¬¬Income Tax band you are in, you may also get up to £1,000 of interest that you don’t need to pay tax on. The £1,000 is 20% of the limit of the interest received from savings, which is £5,000.

DIVIDEND ALLOWANCE: £2,000

If you earn dividends as part of your income, you will only be taxed when those you draw exceed £2,000 in the same tax year. Dividends beyond this amount will be taxed at the following rates:

• Basic rate taxpayers: 8.75%

• Higher-rate taxpayers: 33.75%

• Additional rate taxpayers: 39.35%

It's also important to note that the dividend allowance is in addition to the personal allowance, which is currently £12,570 for the tax year 2022-2023.

Also, if you are a director or an employee of a company, it's important to be aware that dividends you receive from shares in that company may also be subject to tax as employment income.

Dividends allowance is being reduced to £1,000 in the 2023-2024 tax year and £500 in the 2024–2025 tax year.

CAPITAL GAINS ALLOWANCE: £12,300

This is the amount of profit you can earn from selling high-value personal goods before having to pay tax.

Assets jointly owned with a spouse can use the allowances of both individuals, so you can essentially pool your allowances for a total of £24,600 tax free capital gains.

The rates for Capital Gains Tax above the allowance are as follows:

• 10% basic-rate

• 20% high-rate

Capital Gains tax only gains on investments, not the total value of your holding. It applies to most investments held. There are some exceptions such as ISA’s, Investment Bonds or Personal Pensions.

These accounts attract no tax relief, meaning they’re exposed to Capital Gains Tax, and you’ll incur tax on any gain or dividend over your total allowance.

If you do go over the dividend or Capital Gains Tax allowance in a GIA account, you’ll have to sort out the tax yourself through an annual self-assessment return.

For the tax year 2023-2024 the annual exemption amount (AEA) will be £6,000 for individuals and personal representatives, and £3,000 for most trustees.

For the tax year 2024-2025 and subsequent tax years the AEA will be permanently fixed at £3,000 for individuals and personal representatives, and £1,500 for most trustees.

The measure also fixes the CGT proceeds reporting limit at £50,000.

STOCKS & SHARES ISA

You can only add a certain amount of money into an ISA each tax year per person (£20,000 in the tax year 2022-2023).

There are a couple of caveats though. Dividends on non-UK stocks are often subject to local taxes. Those are usually taken at source, and you won’t be able to recoup them, even if you bought the stocks as an ISA.

ISAs also don’t exempt you from paying stamp duty on UK stocks, so be aware of the cost that tax incurs on any purchases you make.

There are different types of ISA available, such as cash ISAs and Innovative Finance ISAs and each one has its own rules and limits. For example, you can only put £4,000 into Lifetime ISA* per tax year.

*only available if you are aged between 18 and 59.

MARRIAGE ALLOWANCE: £1,260

Marriage allowance is a UK tax relief that allows couples to transfer a proportion of their personal allowance to their partner, reducing their tax bill.

This means that if one partner has an income below the Personal Allowance (£12,570 for the tax year 2022-2023) and the other partner pays income tax at the basic rate (20%), the lower earning partner can transfer £1,260 of their Personal Allowance to the higher earning partner, reducing their tax bill by up to £252 for the tax year (£1,260 x 20%).

TRADING ALLOWANCE: £1,000

The UK trading allowance is a tax relief for people who make small amounts of money from trading activities. It allows individuals to earn up to £1,000 per year from trading activities without having to register for self-assessment or pay any income tax on that income.

This allowance is intended for people who run small businesses or sell goods as a hobby, and it applies to all types of trading, such as selling goods online, at markets or car boot sales, or providing services.

However, if you make more than £1,000 from trading activities, you will have to register for self-assessment and pay income tax on the additional income at the rate that applies to you.

FINALLY…

It is important that your planning remains up to date and appropriate to both your needs and current allowances / legislation.

Whether you are seeking growth, income, or a combination of both, it is important that you seek advice from an expert who can review your current position against your objectives and offer advice on anything that may require attention.

Or, if you are interested to hear more about the range of support services we offer our growing community of financial advisers? Get in touch today.